{kind=link}

Whole life policy: A term assurance

plan with an unspecified period, under which sum assured is paid on death.

This plan is mainly devised to create an estate for the heirs of the

policyholder as the plan basically provides for payment of sum assured plus

bonuses on the death of the policyholder

Endowment assurance plan: A term

insurance plan along with pure endowment plan, under which SA is paid on

survival of the specified period or on earlier death. This plan is a

traditional plan and used well by the people to save money. This policy has

paid up value and has maturity value which is dependent on the performance of

the fund of the company but more or less assured.

Money back policy: under which

normally 20% of sum assured is paid on survival every 5 years and 40% on

survival for 20 years and full SA on death at any time within 20 years.

Typically this plan is the combination of 4 pure endowment of varying period

ans 1 term plan for 20 years.

Convertible Plan:

- Convertible plans provide in its terms and conditions, that it can be changed another plan after or within a certain period after commencement

- Example: A term plan can be converted to whole life policy or an endowment policy within a period specified in the original plan. Normally that period is not later than 2 years before the expiry of the original plan

- If the original term insurance cover is for 5 years, the option to convert should be exercised before the end of 3rd year

Advantage:

- No medical examination on conversion

- No further underwriting decision

Such policies are usually

taken by persons in early stages of their career, who expect their financial

condition to improve in future, but would not like to delay the benefits of

insurance.

With Profit and Without Profit Policies

Without profit/ Non-participating policy: Not entitled to bonuses which are declared after actuarial

valuation

With profit/ Participating policy: Premium is slight higher because of the right given to

participate in the progress of insurer. With profit policies are popular

because of the bonuses are expected to be more than the extra premium paid.

Joint Life Policy:

- Two or more lives can be covered under one policy

- Usually cover married couples or partners

- The SA is paid on the death of any of the insured persons during the term or at the end of the term

- Some plans also provide payment of SA on the death of one life and the policy is continued to cover the second life till maturity without payment of further premium

Children Plan

- Insurance is taken on the lives of minor children, proposal will be made by parents

- Risk on the life of the insured child begins only when child attains a specified age

{kind=link}

Deferment period: Time

gap between the date of commencement of policy and commencement of risk.

Deferred date: The

date on which risk will commence. There is no insurance cover during deferment

period. Risk will commence automatically on deferred date. Low premium is main

advantage.

Remember: Life of the children can not be covered

because insurance is a contract and contract with minor is a void contract.

Hence if you practically observe, you will find that in the children plan as

well life assured is of parents.

Riders

- A rider is a clause or condition that is added to a basic policy providing an additional benefit, at a choice of proposer

- Insurers find it convenient to have small number of basic plans, and riders being offered as option

Some of the riders:

1.

Accident death benefit allowing double the SA if death happens

due to accident

2.

Permanent disability benefit

3.

Cover to meet major surgical expense

Annuity Plan

Annuity means a series of payments made at successive

periods or intervals of time is called annuity

Example: salary, loan repayment, SIP

Number of lives covered

Single: provides the annuity to the single

annuitant during his lifetime

Annuitant means the person who buys an annuity plan.

Joint: Payments to be made during the life

time annuitant and his/her spouse and to be stopped on the death of the last

survivor

{kind=link}

Immediate Annuity : If the successive payments are made at

the end of successive period or interval

Annuity Due: If the

successive payments are made at the beginning of the successive period or

interval

The plans offered by the insurance companies are useful for the

people who have retired and are worried about the income stream and longevity.

Annuity Rate:

Amount of annuity payable at yearly intervals which can be purchased for Rs. 1 lakh under different options is as under:

Amount of annuity payable at yearly intervals which can be purchased for Rs. 1 lakh under different options is as under:

Age last birthday

|

Yearly annuity amount under option

|

|||||

( i )

|

( ii ) (15 years certain)

|

( iii )

|

( iv )

|

( v )

|

( vi )

|

|

40

|

7510

|

7440

|

6930

|

5610

|

7310

|

7120

|

45

|

7770

|

7660

|

6960

|

5890

|

7500

|

7240

|

50

|

8140

|

7950

|

7000

|

6280

|

7760

|

7420

|

55

|

8650

|

8330

|

7050

|

6810

|

8130

|

7670

|

60

|

9350

|

8790

|

7110

|

7530

|

8640

|

8030

|

65

|

10410

|

9330

|

7180

|

8590

|

9400

|

8570

|

70

|

12080

|

9830

|

7260

|

10220

|

10560

|

9370

|

75

|

14510

|

10220

|

7360

|

12590

|

12240

|

10590

|

Paid-up

value:

The policy does not acquire any paid-up value.

Surrender Value : No surrender value will be available under the policy.The policy does not acquire any paid-up value.

Loan : No loan will be available under the policy.

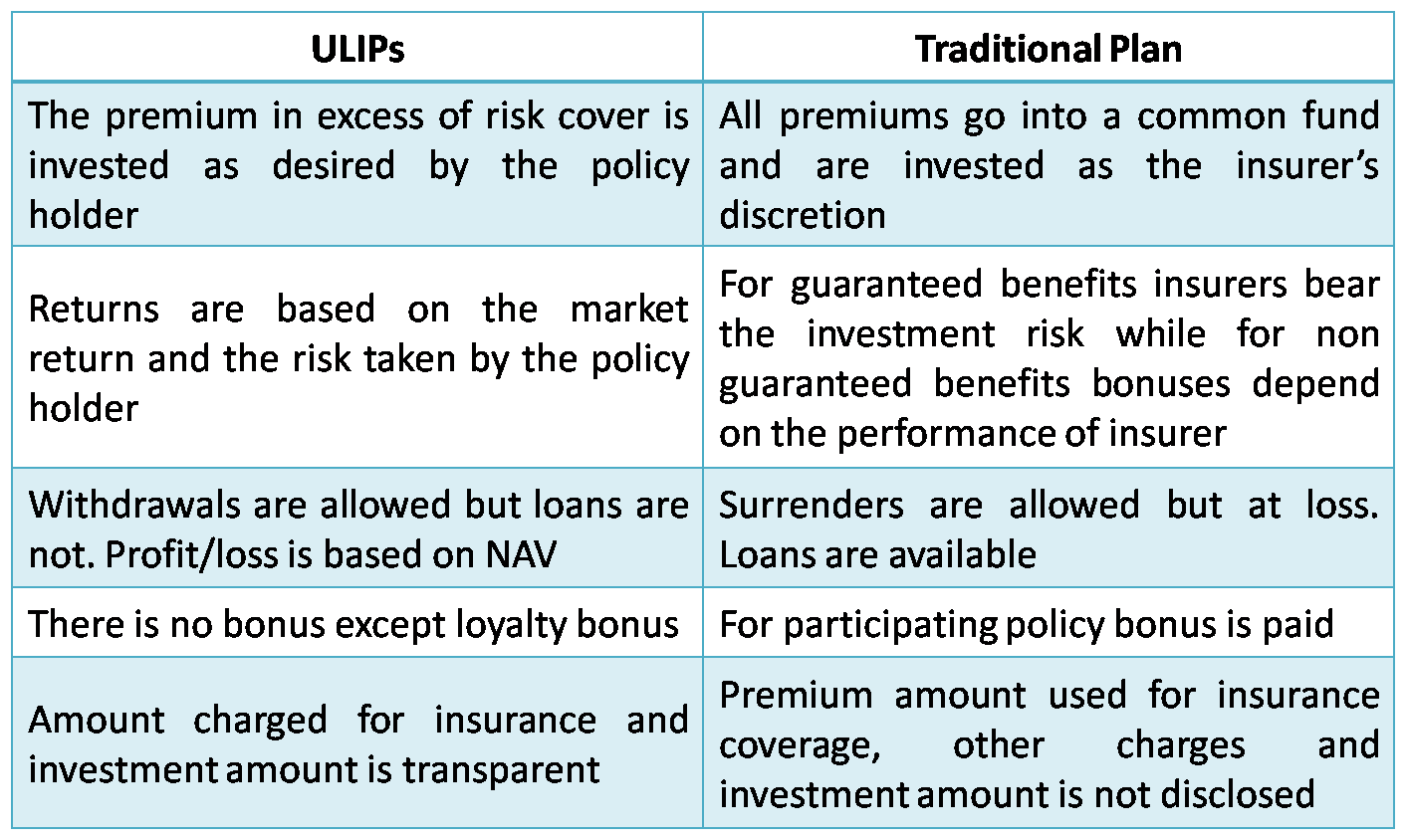

These plans have been of

great success in recent years. It is a hybrid plan which gives an option of

choosing the investment portion to the insured. It combines the benefit of life

insurance as well as giving various options of participating in the growth of the

capital market. The traditional plan of insurance companies never disclose

to insured where his money is invested. This non transparency part is

eliminated by the linked plans. The SA or death cover, payable in the event of

death during the term, is related to the premium usually as multiple like 5

times the annual premium. IRDA guideline: SA has to be 1.25 times for single

premium or 5 times in case of annual premium.

When we talk about

transparency and facilities we should also consider the charges of linked

plans. They are as follows:

1.

Premium Allocation Charge

2.

Mortality Charges

3.

Fund Management Fees

4.

Policy/ Administration Charges

5.

Surrender Charges Service Tax Deductions

Investors may note, that

the portion of the premium after deducting for all charges and premium for risk

cover is utilized for purchasing units.

Lets also understand the

difference between the traditional plans and the linked plans

{kind=link}

Before choosing any life insurance product one must consider the

following:

1. Adequacy

of coverage

2. Cash

outflow/ amount of premium

3. Duration

of need

4. Expenses

of the policy

5. Surrender

charges

However there are several methods to evaluate the various life

insurance policies.

Belth Method

The Belth yearly price of protection method enables to determine

whether a given life insurance policy is competitively priced based on the

annual cost per Rs. 1,000 of protection.

Simply put, it weighs costs against coverage.

The Belth yearly rate of return method allows to determine

whether the rate of return on the investment component of a given policy is

good, fair, or poor.

Try to solve above equation with following:

Post Tax Interest Rate = 12%

Annual Premium = Rs. 10000

Bonus = Rs. 15000

Death Benefit = Rs. 10 lacs

CSV = Rs. 5,00,000

CVP = Rs. 4,60,000

Internal Rate of Return

Commonly used for policy evaluation purposes in business

purchases of life insurance

Surrender-Based IRR

Solves for the IRR/interest rate/yield that causes accumulated

premiums (less any bonus paid)to equal the policy CV at one or more

pre-selected policy durations

Typically, highly negative (with a limit of a negative 100

percent) in early years (short durations) and becomes less negative, and

increasingly positive, with longer durations

Death-Based IRR

Solves for the IRR/interest rate/yield that causes accumulated

“net” premiums to equal the Face Amount at one or more selected policy

durations

In early years (short durations), this IRR will be very large

but declines with longer durations (i.e., the longer the insured lives)